Resilience in the Rann: When Heat Became an Income Risk

Every November, when the monsoon retreats from the Little Rann of Kutch, the land turns into a vast white salt desert. For the Agariya community, this marks the start of six to eight months of salt production under temperatures that often exceed 45°C. India produces nearly 30 million tonnes of salt annually, with Gujarat contributing about 75% of total output. Much of this comes from small seasonal producers in Kutch. For these households, salt is not side income, it is the year’s primary cash flow.

Women do much of this work: levelling pans, managing brine, and raking salt in extreme heat. Many are members of the Self-Employed Women’s Association (SEWA), a trade union of over 2 million informal women workers across India.

Figure 1: Indian salt producers coping with 48°C heat

Source: The Guardian

Rising temperatures began converting occupational hardship into direct income loss. As heatwaves intensified, women lost both workdays and wages. To address this, SEWA piloted a parametric heat insurance cover that automatically triggered payouts once temperature thresholds were breached. When temperatures reached 40°C, women received ₹400; when they exceeded 43°C, payouts ranged between ₹535 and ₹1,800.

The programme eliminated paperwork and loss verification, women did not need to file claims or prove damages. In 2023, the scheme covered more than 21,000 women; by 2024, enrollment had surpassed 50,000.

While the payouts were modest, they arrived immediately. For many participants, that timely liquidity meant avoiding high-interest loans during extreme heat. The weather still turned harsh, but once temperatures crossed the trigger threshold, cash support followed.

When Relief Comes Too Late: The Insurance Gap in a Warming World

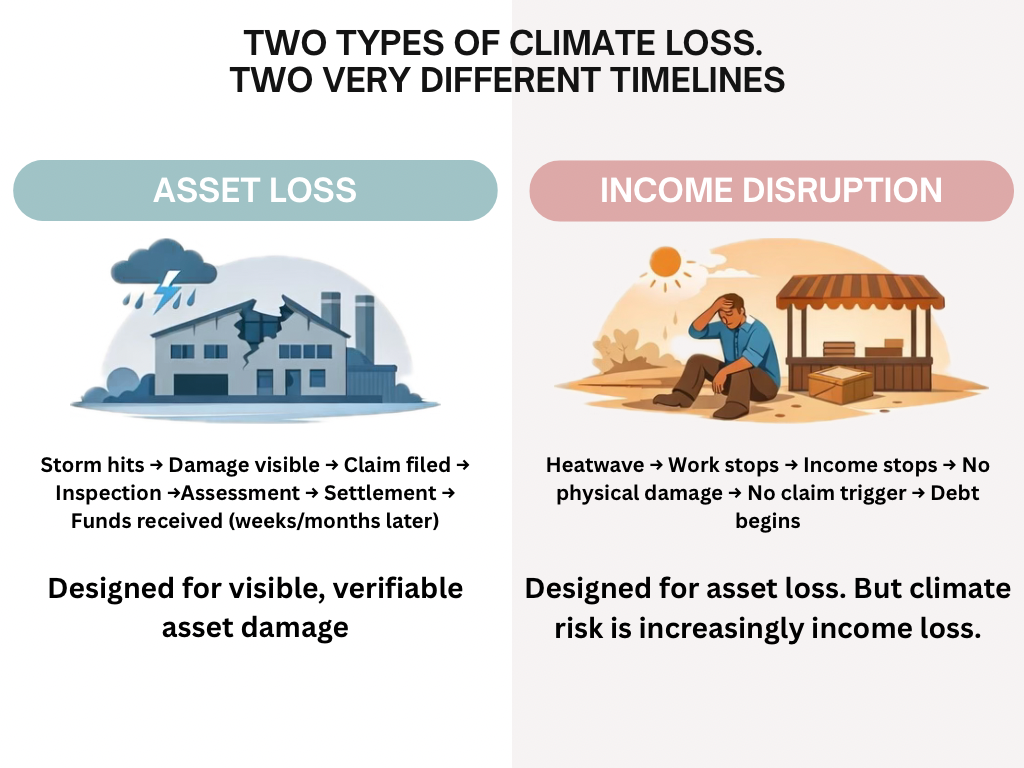

When the salt dissolves, there is no collapsed roof to photograph. No official disaster declaration. Only income that disappears. The dominant form of protection we rely on, indemnity insurance, was built to restore damaged assets. It compensates for proven loss. And that word, “proven,” is where the friction begins.

Indemnity claims follow a structured chain: notification, documentation, inspection, assessment, settlement. That architecture works well for factories, machinery, and buildings. But climate risk today increasingly shows up not as broken infrastructure, but as interrupted income.

Figure 2: The Two Timelines

What does a construction worker document when a heatwave makes work unsafe for five days? What financial record captures dissolved salt or lost street-vendor earnings? For small, frequent losses, the cost of verifying each claim can outweigh the premium itself. Wharton Impact notes that administrative and transaction costs in indemnity microinsurance can “swamp premium revenue” at small scales. The International Association of Insurance Supervisors (IAIS) similarly highlights that managing large volumes of small policies creates disproportionately high claims-handling costs. Meanwhile, over 80% of India’s workforce remains informal (Periodic Labour Force Survey), and non-life insurance penetration remains roughly 1% of GDP (IRDAI Annual Report 2023–24).

The result is a structural mismatch. Climate risk is increasingly income risk, indemnity insurance is built for asset risk. And when liquidity arrives months after paperwork, the financial shock has already hardened into debt. That gap, between the risks people face and the products available, defines today’s protection challenge.

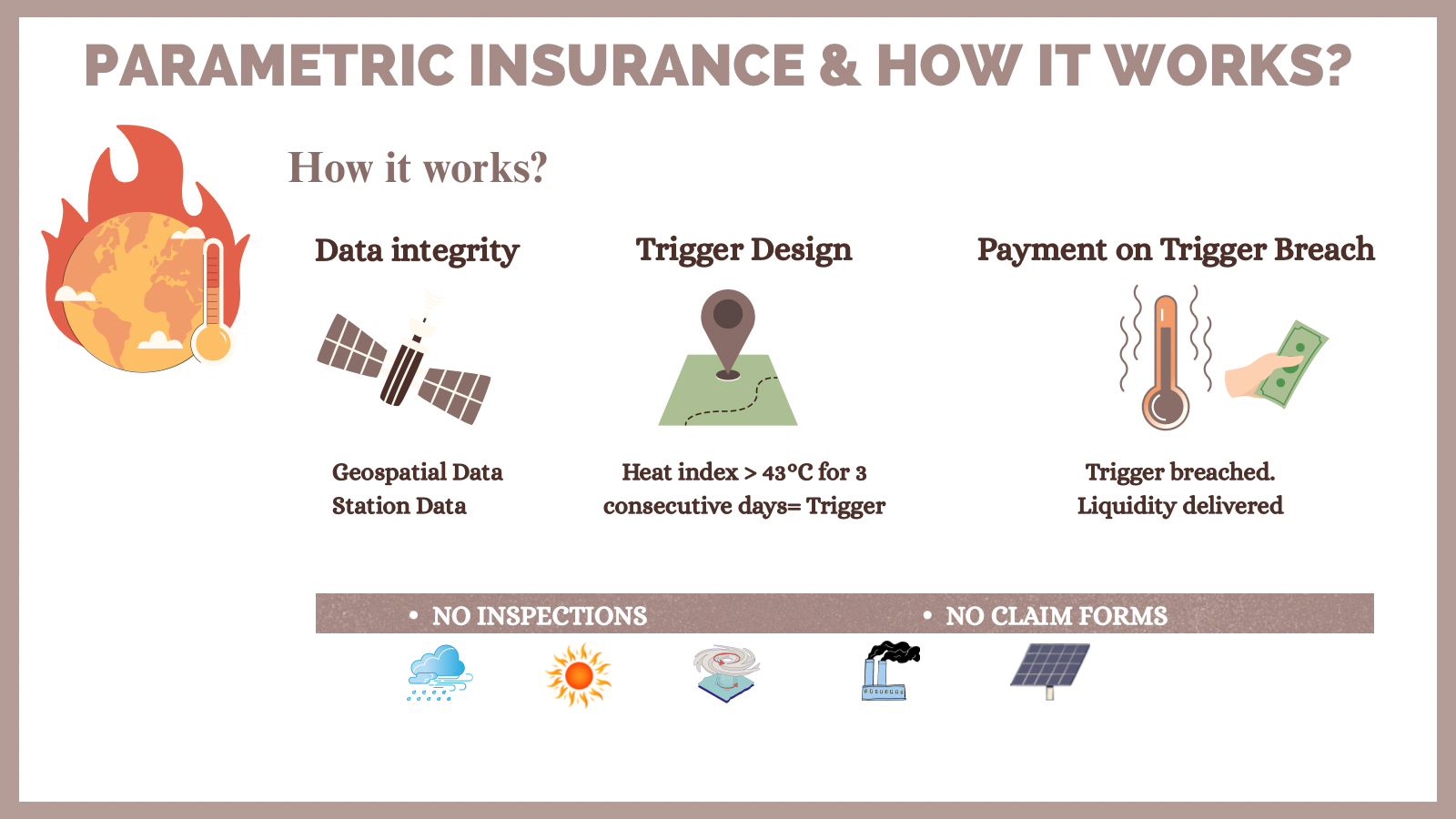

What Is Parametric Insurance ?

Parametric insurance is a rules-based form of risk transfer built around measurable events rather than assessed losses. Instead of reimbursing damage after verification, it pays a pre-agreed amount when a clearly defined environmental parameters; such as temperature, rainfall, wind speed, or river level, crosses a specified threshold. Because the trigger, payout amount, and data source are fixed in advance, the mechanism reduces uncertainty, administrative friction, and settlement delays. In essence, it transforms climate signals into financial signals, converting objective data into immediate liquidity when disruption becomes statistically likely.

Figure 3: Parametric Insurance & How it Works?

How to Design It Well?

Designing parametric protection is not about picking a threshold, it is about engineering credibility. Climate shocks today are frequent and localised, which means triggers must be built from granular hazard-exposure mapping rather than broad averages. Using blended datasets from national meteorological agencies, satellite observations, and global forecast systems, thresholds are calibrated against real economic stress patterns and continuously refined as climate baselines shift. This adaptive design reduces basis risk and ensures that payouts correspond to genuine income disruption.

Equally important is embedding protection where people already operate; within gig platforms, MSME credit lines, cooperatives, and digital ecosystems, so liquidity flows automatically when triggers are breached. In this model, climate intelligence comes first, financial structuring follows, and insurance becomes the final execution layer. Resilience, then, is not reactive compensation, it is pre-designed liquidity delivered at the moment volatility turns into financial strain.

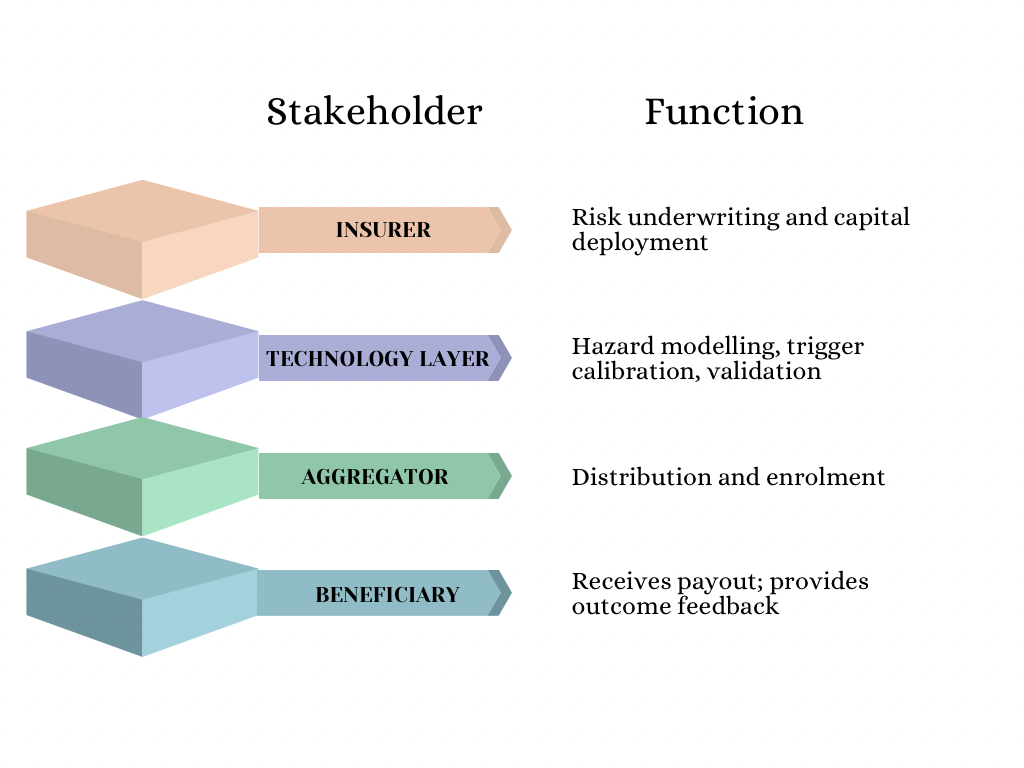

Figure 4: The Parametric Insurance Ecosystem in Practice

If the problem is delayed relief, the solution must be pre-arranged liquidity. Parametric insurance does not ask, “How much did you lose?” It asks, “Did the agreed event occur?” A payout is triggered automatically when a predefined threshold; rainfall, temperature, wind speed, river level, is breached. There is no field inspection, no loss adjuster, no valuation debate. According to the World Bank’s Disaster Risk Financing and Insurance Program, parametric structures rely on independently verifiable data instead of post-event damage assessment, enabling faster disbursement.

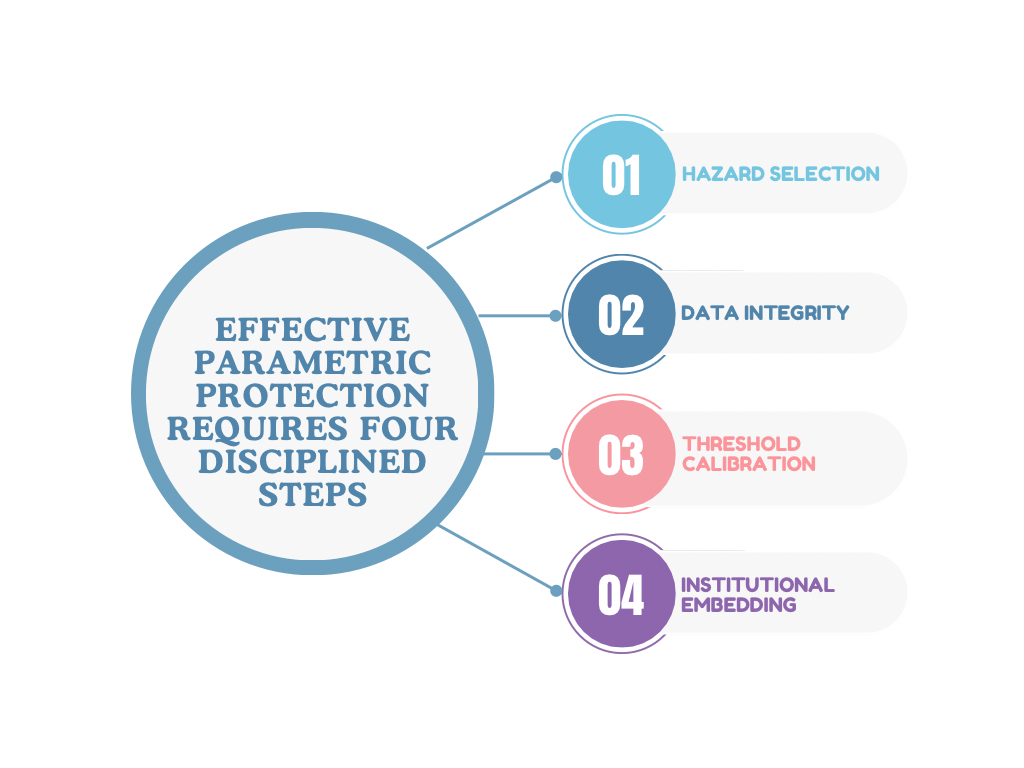

But speed alone is not enough. Design determines credibility. Effective parametric protection requires four disciplined steps:

Figure 5: Design Framework for Parametric Protection

Design begins with hazard selection, identifying measurable climate variables, such as heat index, rainfall deviation, river levels, or wind speed, that demonstrably correlate with income disruption. Next comes data integrity: triggers must be anchored in reliable, independently verifiable datasets, whether from national meteorological agencies, satellite systems, or blended climate models, to ensure credibility. Threshold calibration then links historical hazard patterns to actual economic stress, carefully setting trigger levels that minimise basis risk, the mismatch between a trigger and real-world loss. Finally, institutional embedding ensures the product does not sit in isolation; protection must be integrated into existing ecosystems such as cooperatives, gig platforms, credit systems, or disaster funds so that payouts flow automatically to those exposed.

When designed this way, parametric insurance does not attempt to perfectly compensate every rupee of loss. It stabilises liquidity at the moment of shock. Indemnity restores damage after verification. Parametric protection delivers cash when thresholds are breached. In a climate where risk increasingly manifests as income volatility, that design shift is not incremental, it is structural.

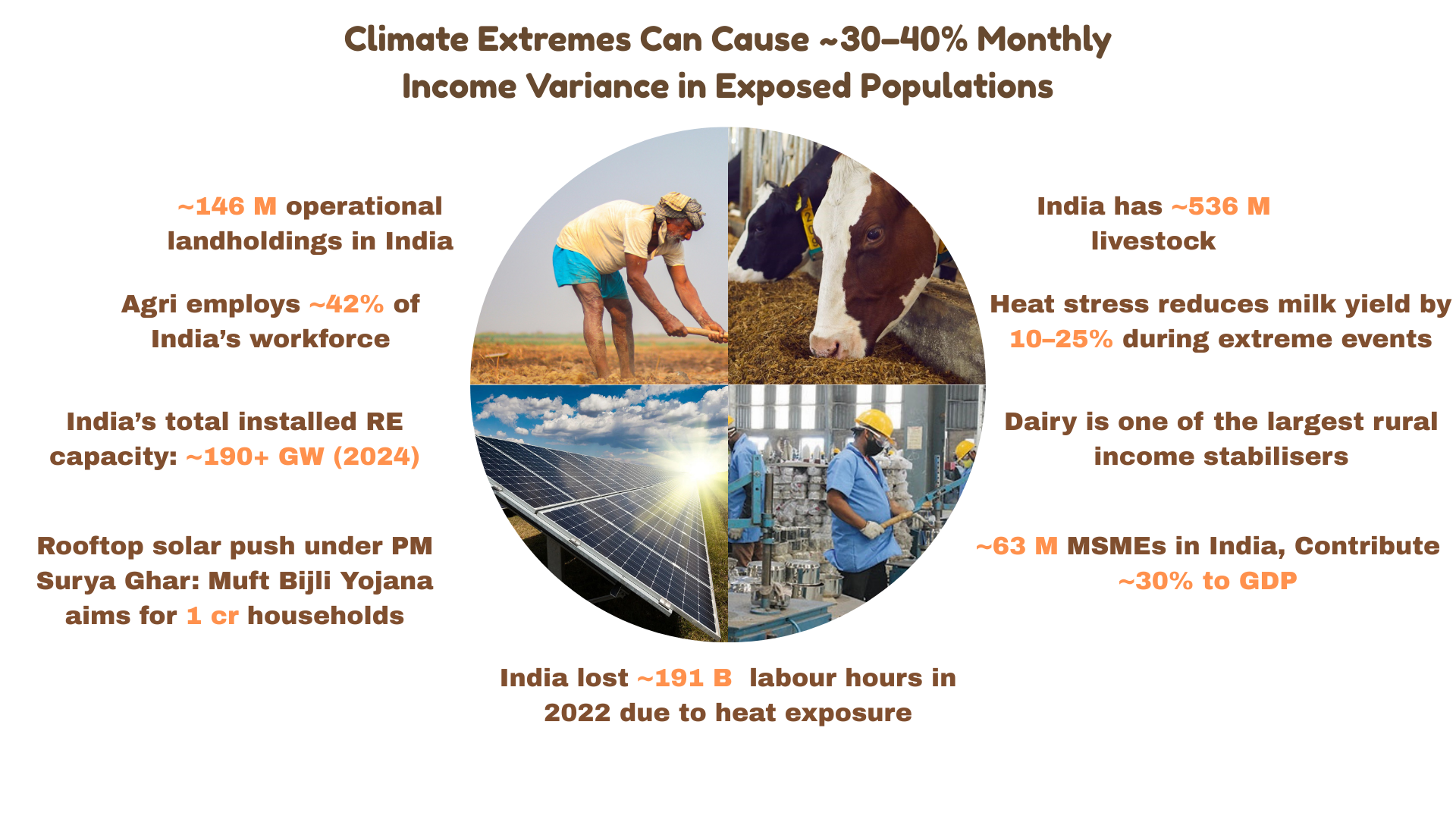

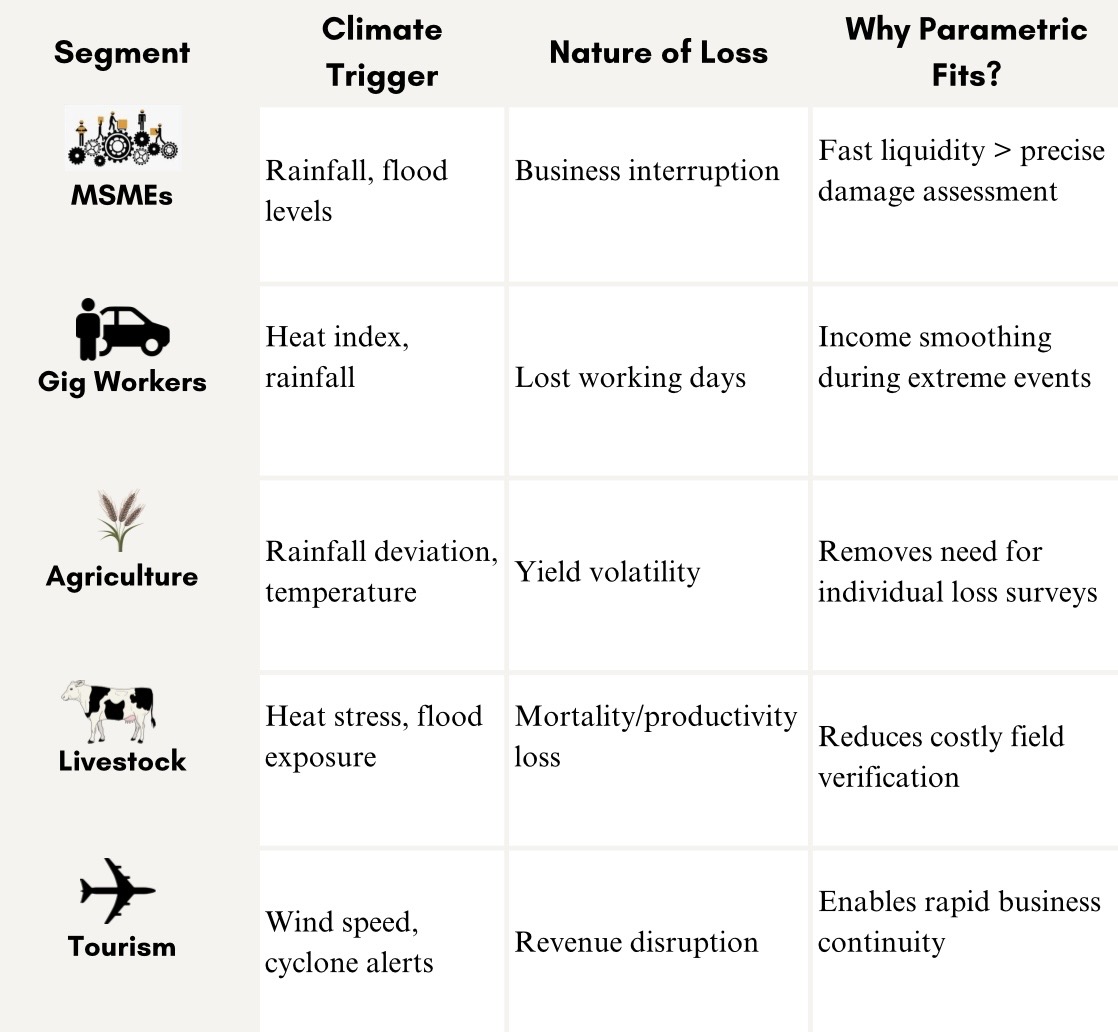

Where It Works: Sectors, Examples, and Market Signals

If parametric insurance is about speed, its true value emerges in sectors where speed determines survival. The first pattern is clear: it works best where losses are frequent, data is available, and cash flow is fragile.

Figure 6: Sectors on the Frontline

What connects these sectors is not just scale, but financial structure. In MSMEs, losses often arise from business interruption rather than structural damage, a factory may remain standing after a flood, yet cash flow stalls while wages, rent, and supplier payments continue. During the 2018 Kerala floods, total losses were estimated at ₹31,000 crore, and many small enterprises struggled with prolonged downtime despite intact premises.In platform-based work, income stops the moment conditions become unsafe; with India projected to have 23 million gig workers by 2030, heat exposure is increasingly a balance-sheet risk, not just a health concern.

Weather-indexed models such as India’s Weather-Based Crop Insurance Scheme (WBCIS) already demonstrate how rainfall and temperature triggers can reduce assessment delays. The same logic extends to livestock and renewable energy, where productivity and generation depend directly on measurable climate variables. Across these segments, parametric insurance is less about compensating visible damage and more about ensuring liquidity when revenue is disrupted, often determining whether recovery takes days or an entire season.

Table 1: Where Parametric Insurance Works Best

The Market Opportunity

Three structural forces make this market significant:

- Vulnerability: South Asia is among the most climate-vulnerable regions globally (IPCC AR6).

- Scale: Over 400 million informal workers across the region.

- Underinsurance: Non-life penetration in India remains roughly 1% of GDP (IRDAI).

When climate volatility intersects with underinsurance at this scale, the addressable need is enormous.

Why Does it Matter for General Insurers?

India’s non-life insurance penetration remains low at roughly 1% of GDP, with portfolios still heavily concentrated in motor and health insurance (IRDAI Annual Report 2023–24). In a climate-exposed economy, this leaves a significant protection gap, and a clear growth opportunity.

✓ A Large, Underinsured Market

Climate-linked income risk across MSMEs, gig workers, agriculture, livestock, and renewable energy remains largely uninsured. Parametric insurance opens access to these segments where traditional indemnity models are inefficient.

✓ A New Product Class, First-Mover Advantage

Parametric structures represent a distinct, data-driven product line. Early movers can shape underwriting standards, build ecosystem partnerships, and position themselves as leaders in climate risk financing rather than compete in saturated lines.

✓ Portfolio Diversification, Not Just Exposure

While correlated payouts are a concern, risk can be mitigated through hazard diversification (heat, rainfall, wind, air quality), geographic dispersion, and layered reinsurance, building a balanced, trigger-based book.

✓ Digitally Scalable by Design

Parametric covers can be embedded into lending platforms, gig apps, agri-tech systems, and renewable energy financing structures, enabling low-cost distribution through aggregators and digital ecosystems.

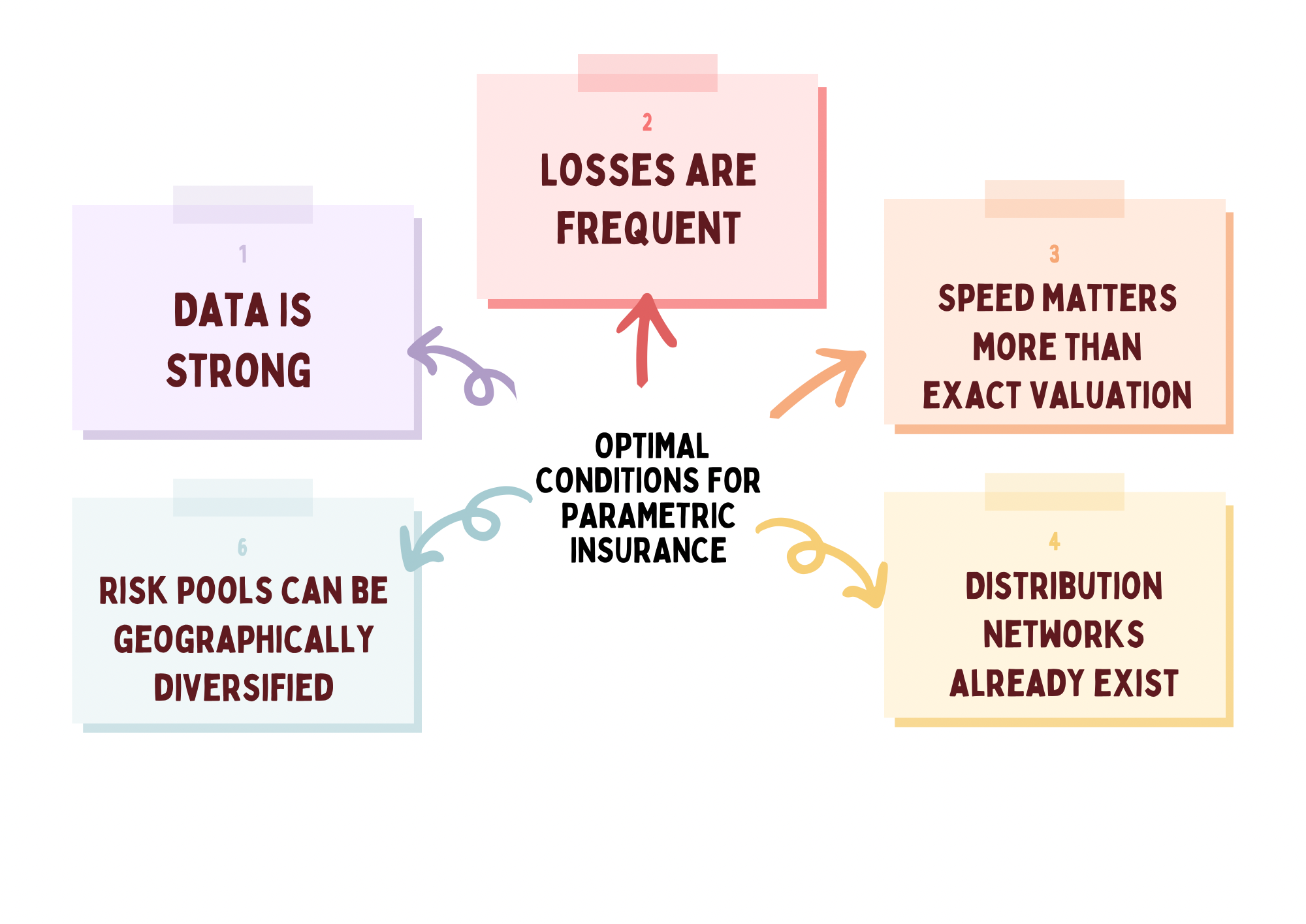

Figure 7: Optimal Conditions for Parametric Insurance

In other words, it works best in precisely the segments most exposed to climate volatility. And that brings us to the next layer of the conversation: technology. Because parametric insurance is only as credible as the data and modelling behind it.

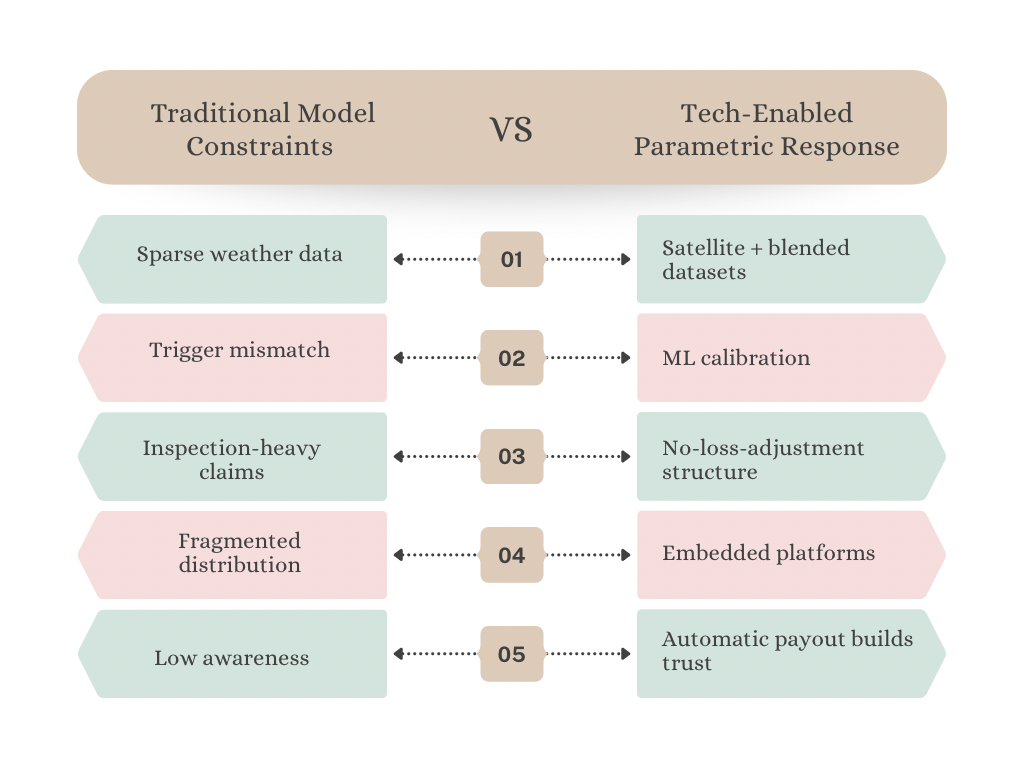

Figure 8: “Old Model vs New Model” Comparison

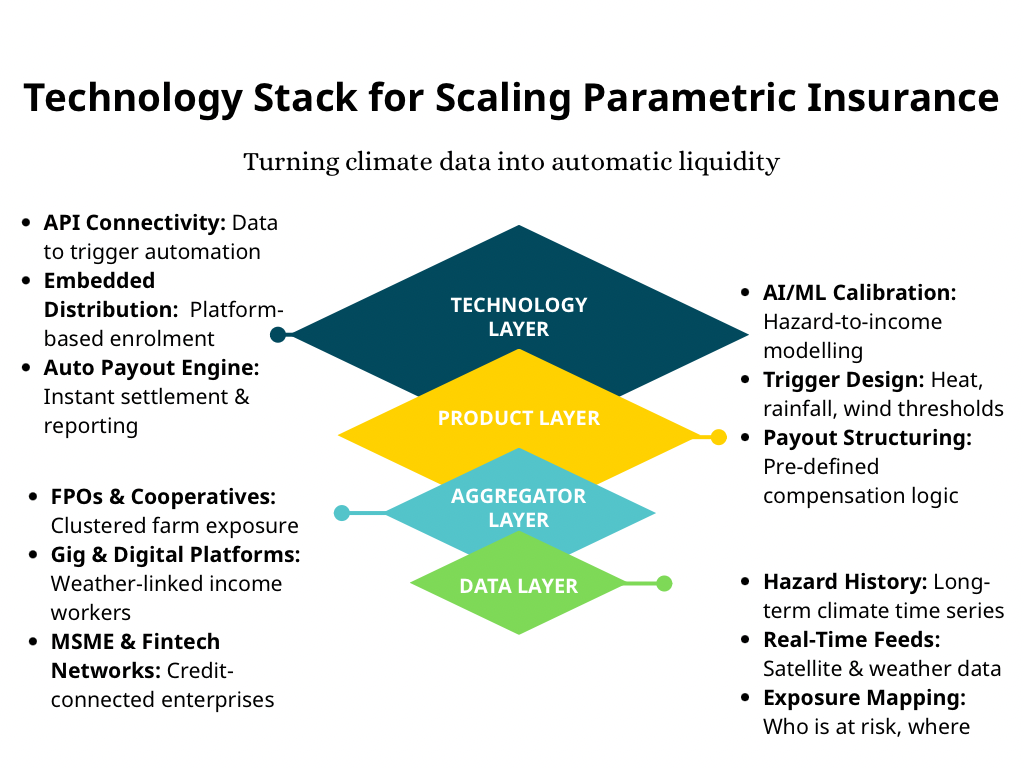

Technology Stack for Scaling Parametric Insurance

Figure 9: End-to-End Technology Stack for Parametric Insurance

Parametric insurance scales only when data quality, scientific calibration, and distribution intelligence move in sync. The challenge is not access to information, but credibility, ensuring that thresholds reflect real economic stress and evolve as climate baselines shift. Advances in satellite observation, global forecast models, and geospatial computing have transformed weather data into a reliable financial input. But data alone is insufficient. Trust depends on minimising basis risk, aligning triggers with observed income disruption, and embedding products within ecosystems that already serve vulnerable populations. When climate science, actuarial logic, and digital distribution operate as a unified system, parametric insurance shifts from pilot innovation to scalable infrastructure.

Scaling Beyond Pilots: From Demonstrations to Durable Protection

Parametric insurance in India is no longer theoretical, but scale remains the real test. One early lesson comes from Nagaland’s Disaster Risk Transfer Parametric Insurance Solution (DRTPS). In 2021, Nagaland became the first Indian state to pilot a rainfall-triggered parametric cover in partnership with Tata AIG and Swiss Re. The policy was designed to strengthen the State Disaster Response Fund by triggering payouts when rainfall crossed predefined thresholds.

However, despite heavy rainfall and flooding, payouts were not triggered because the dataset used for threshold calibration differed from local IMD measurements. The lesson was immediate: credibility in parametric insurance hinges on data alignment.

By 2024, Nagaland had signed a new agreement with SBI General Insurance, expanding coverage to ₹150 crore and revising trigger parameters. Meanwhile, SEWA’s parametric heat cover illustrated how well-designed triggers can deliver rapid payouts to informal workers. In 2023 alone, more than 21,000 women received automatic compensation after temperature thresholds were breached.

Kerala’s dairy cooperative MILMA also moved in this direction, partnering with the Agriculture Insurance Company of India to introduce a heat-index cover for livestock in 2023. During its first year, ₹29 lakh in claims were disbursed against ₹6 lakh in premium collected, a strong indicator of operational viability.

These pilots highlight both friction and feasibility. Scaling parametric insurance demands robust data systems, carefully calibrated triggers, regulatory clarity, and deep institutional integration. Absent these foundations, pilots remain experiments; with them, they evolve into critical resilience infrastructure.

From Risk Awareness to Financial Readiness

Climate risk is no longer distant or rare. It is embedded in everyday economic life, from salt pans in Kutch and dairy routes in Kerala to factory floors in Coimbatore and delivery networks in Guwahati. We often frame climate risk as an infrastructure problem; stronger embankments, better drainage, improved forecasting. All of that matters. But the deeper vulnerability is income disruption. The shock may not always be visible. The financial stress is immediate.

Parametric insurance does not replace long-term investment or indemnity cover. It does something precise and powerful: it delivers timely liquidity when thresholds are triggered, preventing temporary shocks from spiralling into debt, distress sales, or lost opportunity. Increasingly, global institutions are championing pre-arranged, rules-based financing that shifts disaster response from reactive relief to planned resilience.

This is not a niche solution, it is a large structural opportunity. Customers gain stability. Insurers and reinsurers access diversified, data-driven portfolios. Aggregators unlock new markets. The broader ecosystem strengthens through better risk distribution. The need of the hour is scale. Climate volatility cannot be managed manually or locally. It requires deep tech, granular data, automated triggers, and portfolio-level risk distribution to make protection affordable and sustainable.

The greatest danger in times of turbulence is not the turbulence; it is to act with yesterday’s logic.

~ Peter Drucker